I was trying to find a short read on why economic growth is so important, but since it wasn’t readily available, I decided to collate one myself. To do so, I’ve borrowed liberally (and literally) from Our World in Data and Tyler Cowen’s Stubborn Attachments, which are much better (but also longer).

When you look at economic history, it’s a very simple story with only two parts:

The first part is the very long time in which the average person was very poor, life expectancy was low, and child mortality rate was high.

This lasted through most of history. What people used for shelter, food, clothing, and energy stayed basically the same for a very long time. If you lived during the 17th century, for example, your quality of life was pretty similar to those who lived a thousand years earlier.

The second part is much shorter — a time in which average incomes grew rapidly.This was the time when we first experienced economic growth.

Before this, population density determined living standards — the economy was zero sum. More people meant fewer resources per person. More births meant lower incomes; more deaths meant higher incomes.

The latter actually happened during the Black Death, which killed 8% of the population, but left survivors better off. Indeed: The economy was a zero-sum game where the death of others meant more resources for everyone else.

This zero sum dynamic is what Malthus feared would exist in perpetuity — that any increase in productivity would only increase the population size, leaving no change to living standards. Thus, poverty would always remain the condition of the masses.

This is why there was resistance to help the poor in pre-growth times, because the concern was they’d have more kids, and that would make everyone else worse off.

Then from around 1685 in England (and soon everywhere else) onwards, population size and income per person started growing in tandem. We had officially escaped the Malthusian Trap.

As we now know, Malthus was right about describing our past (or the present, from his perspective), but he was wrong about the future. He failed to appreciate how productivity growth would mean that higher populations would drive higher incomes & better living standards for all.

Indeed: It was now possible for population and income to rise in lockstep. Before that, technological growth only produced more people, not richer people. Economic growth meant population growth and rising prosperity could go together.

It’s hard to understate how much economic growth has improved our standard of living. The average person in the world is 4.4-times richer than they would have been in 1950, and over that same time period, the world has 3x’ed population. If growth didn’t increase along with the population, everyone in the world would be 3x poorer than they would have been in 1950.

And yet we still don’t intuitively understand this.

Russ Roberts once asked journalists how much they thought we’ve improved economic growth since 1900, and they said about 50%. In reality, the answer is about 5 to 7 times.

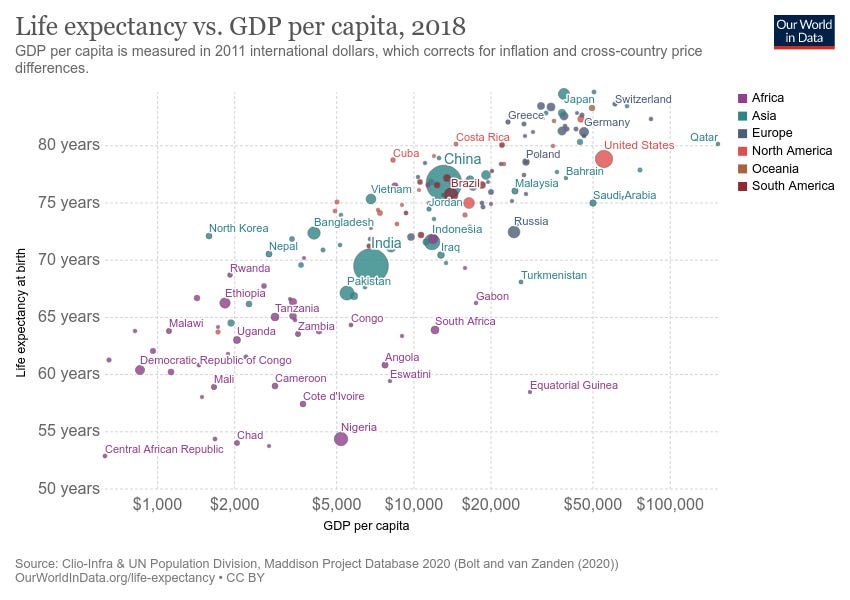

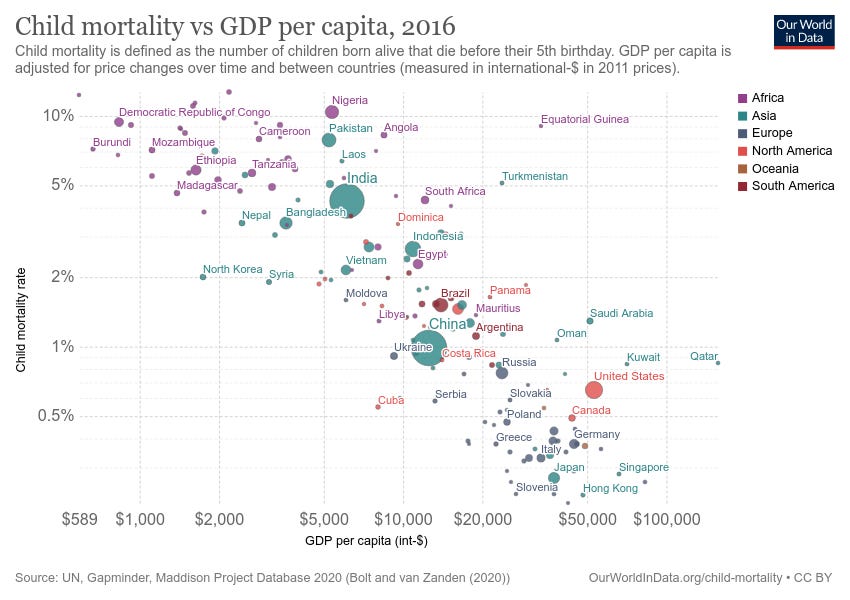

Economic growth is positively correlated with almost every measure we care about. People with higher living standards live longer lives, suffer less pain, recover better from trauma, etc. The richer the population, the happier and healthier it’s people are. Just compare Cuba & Singapore to see:

Even small amounts of economic growth can have enormous impacts. If you take a time period of about 100 years, and you have the American economy grow one percentage point less each year over that time, we would today have the national wealth of Mexico, not the United States.

Tyler Cowen expounds:

“Extra wealth also serves as a cushion against very bad events, or at least against later declines in wealth. Ten or fifteen years ago, it was common to hear the claim that once a nation reaches the level of material wealth found in Greece, happiness more or less flatlines. Indeed, this was more or less where the flatlining point seemed to be. Yet since the Greek economic crisis, dating from 2009, no one uses the Greek example to make a point about the flatlining of the happiness-income relationship. The country lost almost a quarter of its economic output, unemployment has risen to over twenty percent, there have been riots in the streets, a neo-Nazi party was elected to the legislature, and at times basic medicines have been unavailable. Having some additional reserves of wealth prior to the crisis would have helped the country a good deal, and might have prevented the troubles altogether by easing debt repayment.”

Tyler’s book, more broadly, is an argument for why pursuing economic growth is a moral imperative for our society. He inverts Rawls argument: if Rawls says we should maximize growth to make the worst person better off, Cowen says we should redistribute wealth only so long as it leads to economic growth (since growth is what expands the pie/increases wealth to begin with).

In a world where we optimize for economic growth (with caveats for respecting human rights and environmental sustainability), some people are worse-off short-term, but all are better off long-term, as evidenced by how people live today vs. 100 years ago.

Cowen’s conceit is if we sacrifice economic growth today, we’re stealing from future people — and we should obviously care about our future children.

Indeed: Rawls’ Veil of Ignorance takes into account where you were born, but not when. If it did, you’d prioritize anything that promoted economic growth — because if you didn’t, you’d be effectively stealing from future people.

Redistribution can be a one-off effect where economic growth compounds, and yet people don't fully appreciate it. When we redistribute wealth in a way that sacrifices economic growth, we're also redistributing resources away from our future children. The key lesson? Good redistribution is about increasing growth, not the opposite.

This begs the question: if economic growth is so obviously good for us, why is it unpopular?

Well, first off, capitalism has no PR department. Our government takes credit for private gains, even though the private sector’s growth is what supports government transfers in the first place.

But because these transfers come from the government itself, people fail to make the much needed connection back to private enterprise. We say billionaires shouldn’t exist, but we don’t mind the government itself being a trillionaire because of the illusion of accountability: though 90% of the government isn’t elected, they still get moral high ground.

To fix this, CEOs and their corporations need to make their societal impact legible. Maybe we tie UBIto the S&P? This would align incentives such that when corporations get rich, people do too.

Or maybe a better way to redistribute wealth is to broaden equity ownership to everyone. If people use Facebook, for example, perhaps they could earn equity in the company as a result of being a daily active user of their product.

We underestimate the psychological effects of equity — it aligns everyone on the way up (unity) instead of letting them fight for scraps on the way down (divide).

So if we agree that equity ownership & economic growth are positive externalities on the world, then the demonization of billionaires argument is misguided. When people get rich in a sustainable way, we should celebrate them, because, among other reasons, some of that money goes to the government, which (hopefully) means more education, healthcare, and other programs.

Without growth, however, we wouldn’t be able to pay for these services. Each public job is in effect “sponsored” by a private job via taxes.

Indeed, a lot of capitalism is just unintuitive. It's tough to explain how a minimum wage won’t help someone who’s making $8 an hour. It's tough to explain compounding returns. We’re evolved for a zero sum world that Malthus predicted would continue, and we still haven’t internalized that the economy is now positive-sum.

Capitalism hasn’t been portrayed inspiringly — a system with the pursuit of self-interest as its guiding light doesn’t exactly nourish the soul.

By contrast, communism & socialism are very inspiring, calling for the best of humans and resonating most with how we relate to our friends and family ("From each according to his ability; to each according to his needs").

Since communism is the approach we take with our families, we assume it should also work at scale. And since capitalism is the opposite — unnatural within families — the fact that it feeds billions of people is counterintuitive.

This is how you get global corporations promoting Marxism.

Indeed: during the Spanish Civil War, soldiers were said to have died with the word "Stalin" on their lips. We don’t see people dying with “free markets” on their lips...

This presents an opportunity: How do we make capitalism more popular?

In 2019, Patrick Collison and Tyler Cowen presented their case for why Progress Studies should be an academic field. The explicit idea was to help us study how institutions and cultures lead to more economic growth, while the implicit idea was to raise the status of economic growth in the process.

This has often been contrasted with transhumanism as an approach to popularize technological growth. They’re both responses to the failure of liberalism/libertarianism to support pro-growth policies towards immigration, free-trade, or lower government spending.

People need a mission, and so perhaps the Progress movement needs to go one of two ways to resonate with a wider audience. It should either lean into futurism (space, longevity, etc) or moral authority (ending poverty). The only options are "let's end poverty for all" or "let's end death for all". Of course, we could do both, it’s just a matter of emphasis.

More broadly, I wonder if a cultural ethos/movement around “positive sum” would resonate widely. It’d recognize our increasingly intertwining fates, the importance of expanding and sharing the pie, and the need to refocus our attention towards abundance rather than scarcity, envy, and status games.

The movement would need to concede how unintuitive capitalism is, and acknowledge that positive-sum thinking is a learned behavior. It would have socialism on a local relationship and community level (which provides priceless connection and reciprocal benefits, while being inefficient with no metrics/scale), and capitalism on a global level (a world with market-based prices, comparative advantages, optimization, scale, and wealth creation).

It would need to have a vigorous defense of technology, especially since society survives or dies based on its ability to sustainably grow the pie. Without a growing pie, there’s a winner for every loser, and we engage in zero sum conflict. The bigger the pie, the more there is to redistribute as well. Technology innovation, if done well, helps do more with less—growing the pie without hurting the environment.

In the coming weeks we’ll dive deeper into some central questions around what causes and hinders economic growth.

Until next time...

Read of the week: Alex Kaschuta on Gatekeeping

Listen of the week: Jim Rutt and Samo Burjia

Watch of the week: Jesse Walden on Means of Creation

Cosign of the week: Bitclout is ingenius (the mechanic of stock investing in people, separate from their specific implementation and surrounding controversy), I just can’t believe I didn’t think of it first. We are doubly inspired to bring Cosign back, maybe it should have an economic component as well.

On Deck Updates:

We launched On Deck Miami w/ Keith Rabois which will take place during May

I’m hiring a Chief of Staff for On Deck, and also an EA.

We’re hiring a Thinker in Residence who will help incubate this idea—a personal trainer for intellectual growth. Reach out if appropriate.

Until next week,

Erik

One effective way to promote capitalism could be telling more success stories (startup founders, creators of all kinds, etc) in a way that is _relatable_. This gets to the heart of enlightened self-interest and makes it very clear that such stories wouldn't be possible under the alternative system.

But then again, no matter how much opportunity there is, some people will always be left behind for many reasons — one of them is sheer luck. And they will always feel that the system is unfair. So another strategy to make sure that the worst (think 1918 in Russia) would not happen is to ensure a proper safety net and prevent inequality from getting too much out of control.

On a related note: you might be interested in this blog post that explores what metrics other than GDP we might want to measure and regularly report on: https://max2c.substack.com/p/the-national-dashboard-and-human

I agree without robust private enterprise, there would not be a strong tax base to support the government. But is it not a two way street? Why do corporations and CEOs not give credit to the government for creating the environment for their success? Do CEOs owe nothing for the benfit of operating a company in a rules based society, with strong property and contract protection laws, unbiased courts, a well functioning capital market? Do compannies not owe thanks to the government for educating many of the employees that allow their companies to function and compete?