Will the United States be forced to use inflation to reduce its debt?

A summary of the podcast discussion with Lyn Alden and Scott Sumner

Note: This is a niche & wonky summary. Future posts will be less like this.

This post summarizes the talk I hosted between Lyn Alden and Scott Sumner on the Venture Stories podcast this January. It also references earlier posts on Lyn’s Devaluing the Dollar thesis and Scott’s Market Monetarism camp. In the podcast, we discussed Lyn’s assertion that the US will use inflation to devalue its $29 trillion debt, the similarities, and differences between the debt situation in the 1940s and today, and how countries can monetize debt. We also discussed why interest rates have remained low, if and how the Fed can keep inflation at bay, and the transitory inflation hypothesis.

You can find the audio of the debate here: Part 1 Part 2

The Staggering Size of the US National Debt

Chart source: St. Louis Fed

The US federal debt has been growing since the 1970s and is now surpassing $29 trillion in 2022. The debt has increased dramatically in the last two years, driven by massive stimulus meant to ease the US through the pandemic-driven recession.

Not only has the national debt increased in absolute terms, but the debt-to-GDP ratio has also increased, recently eclipsing 130%. Although both Sumner and Alden agree that our debt is too large, they do not agree on what the United States will do about it. Lyn believes that the United States will be forced to use inflation to devalue our national debt. Scott is skeptical that inflation can be used to reduce the debt in a meaningful way, and expects that we will have higher taxes and austerity in the future to reduce the total level of debt.

We’ve been here before. The 1940s as a model for today's debt situation.

Alden and Sumner both agree that the best model we have for today's debt situation is the 1940s, with the caveat that Sumner believes in some respects, our situation is worse.

In the 1940s the United States had a high debt-to-GDP ratio along with significant private debt. We had an external shock to the economy (WWII), and we had policy coordination between the Federal Reserve and the President/Congress. There was a positive inflation target, and the central bank bought large amounts of debt. Today, we have all of these same conditions, the only difference being that we are experiencing a pandemic shock, and in the 1940s, we experienced a war shock.

Scott believes today’s situation is worse than in the 1940s because WWII was a one-time event. The United States was not running persistent deficits before and after the war, and the deficit was for a specific purpose, not for general spending. Because of this, the debt ratio came down quickly after WWII. Today we not only have to run large deficits (about 100% of GDP), but we also face future deficits that are higher than we experienced in the post-WWII period.

How will the US reduce its debt in the future?

Lyn is convinced that the US will have to inflate its debt away.

Her belief rests on Ray Dalio’s concept of the long-term debt cycle. To understand Ray Dalio's Long Term Debt cycle, we must first understand the short-term business cycle.

During market expansions, public and private debt increases as a percentage of GDP. There are more opportunities to utilize debt to make money in a bull market, and people are optimistic about the future. During this phase, people take out more loans and use more leverage.

Eventually, an external catalyst causes the bull market to end, resulting in a deleveraging or a recession. This process describes the 5 to 10-year credit cycle, which is the regime we've had for many decades.

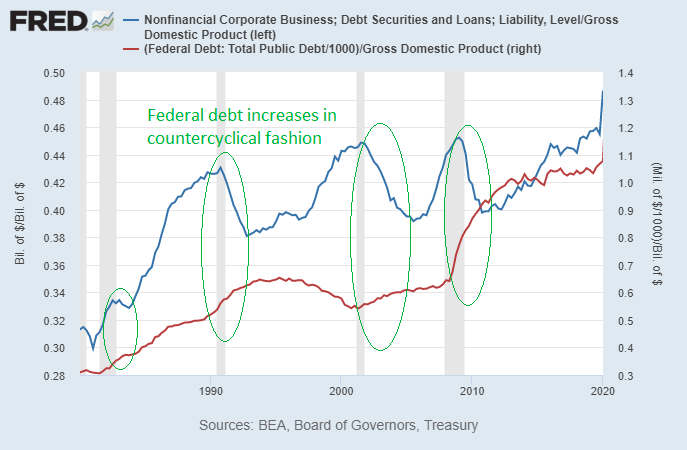

In response to a recession, policymakers cut interest rates and do fiscal stimulus. However, this is a problem because before we can deleverage down, the bull market starts again. In this way, you can string together multiple credit cycles, and, over time, you end up with higher and higher debt to GDP ratios. You get higher highs and lower lows of debt as a percentage of GDP. You can see this phenomenon on the chart below.

Chart source: St. Louis Fed

This cycle continues until interest rates hit the zero lower bound or slightly below it. When you hit the zero lower bound, you can no longer rely on monetary policy to pull you out of a recession. The zero lower bound is a macroeconomic problem that occurs when the short-term nominal interest rate is at or near zero, causing a liquidity trap and limiting the central bank's capacity to stimulate economic growth.

This describes what happened in the 1940s, and in response, we turned to aggressive fiscal policy instead of monetary policy. The government ran enormous deficits while the central bank held interest rates low. In this way, we could deleverage some of the debt while limiting how much debt was nominally in default. You inflate some of the debt away, and the currency gets devalued. This describes our current situation.

Lyn found that countries used inflation to reduce their debts in 52 out of 53 situations where the debt to GDP ratio was as high as it is in the US. their debt away. Scott isn’t so sure that this is a useful signal. He believes that there is a lot of correlation between countries. For example: Under Bretton woods, most countries had the same inflation rate. He thinks we need to look at the US on its own terms.

Scott’s isn’t so sure that it is possible for the US to use inflation to meaningfully reduce its debt.

He thinks austerity and higher taxes are a more likely solution to the debt crisis. He lists three ways that it is possible to use inflation to reduce debt, and he believes none of them work well in practice.

The first way is to increase the price level dramatically to reduce the real value of existing long-term bonds. The US tried this after WWII by issuing 30-year bonds at low-interest rates, after which prices began to rise sharply. This caused the real value of the debt to fall, and the debt became easier to pay off. If the United States were to use inflation to reduce its debt, it would likely do so in this manner. The constraint on this approach is that you can only do it once because the market will then avoid long-term bonds, which could be devalued in this way.

The second way, which economists call seigniorage, is to buy bonds to increase the money supply and run persistently high inflation. This allows you to create tax revenue through inflation. seigniorage works, but it is difficult to use it to raise meaningful amounts of revenue unless you run very high inflation rates. The maximum amount of revenue you can expect to raise with seigniorage is maybe 4% of GDP, an inconsequential number when you understand we're facing debts of 131% of GDP.

The third way to use inflation to reduce debt is to hold interest rates below inflation. Many economists (including Scott) do not think monetary policy can artificially hold interest rates below inflation in the long run. It looked like they were doing it in the 1940s, and it seems like they are doing it today, but in reality, it's just the equilibrium interest rate falling to a very low level.

Scott believes the US is unwilling to accept the inflation level required to make any of these tools meaningfully reduce the debt. Instead of using inflation, it is more likely that the US will turn to austerity and more European-like tax levels in the future to pay down the debt.

Can the Federal Reserve prevent inflation?

Scott believes that the Fed has plenty of tools to fight inflation if it wants to.

Broadly, the Fed has two options in how it can fight inflation. One option is to pull the money out of circulation through open market sales. The other option is to raise the interest rate on reserves so that more reserves stay in the banking system and don't go out into the broader economy.

He thinks two things would have to happen for inflation to get out of control where the Fed loses the ability to combat it. He considered these both less than 50/50 propositions.

First, equilibrium interest rates would have to rise substantially – this is unlikely because they have been trending down for 40 years. Second, fiscal authorities (Congress/the President) would have to bully the Fed into allowing inflation rather than raising taxes to avoid defaulting on the debt.

Lyn believes the Fed's tools to manage inflation are more limited today than in the past.

Why? Today, inflation is coming from the fiscal side and from the fact that banks have not lent out much money vs. their reserves (i.e., there is a low money multiplier effect). The monetary multiplier effect occurs when banks lend more than they hold in deposits and the increase in the money supply exceeds the initial deposit amount. Because the money multiplier effect is already low, the Fed has less room to raise interest rates on reserves to encourage banks to pull money out of the economy. When the Fed raises interest rates on reserves, it decreases the amount of money in the system because it incentivizes banks to lend less money.

Additionally, she notes that the foreign sector is buying fewer treasuries than in the past. If the Fed stopped buying treasuries, they would run into a supply/demand issue that would push treasury yields up. For example, if you have $30 trillion in national debt, you would have a trillion dollars in interest payments if you keep interest rates at 3%. The level of bank reserves and the rate of fiscal spending are two things that the Fed does not have control over, and Alden thinks these will be more important for inflation going forward.

Is our low interest rate environment natural?

Scott believes that we will have a persistently low-interest-rate environment in the future but that it is plausible that interest rates may rise again.

He believes that the low-interest rates we are experiencing are natural and that if the interest rates were artificially depressed, we'd be experiencing much more inflation. The equilibrium level of interest rates seems to be fairly low today. He doesn't quite understand why this is: it might be because of higher global savings rates, the information economy requires less physical investment, or it may be because of an aging population.

What is the relationship between central bank purchases of public debt and interest rates? It’s complicated. In a direct sense, if you buy debt, that pushes prices up and lowers the yield. On the other hand, there can be powerful forces pushing the prices down over the medium to long term.

For example, in the 1960s and 1970s, the long-term effect on inflation was so powerful that the Fisher effect overwhelmed the liquidity effect of buying bonds, which in the short run lowers interest rates. The hypothesis that we will eventually have a lot of inflation because we're going to have a lot of debt monetization from the Fed is a hypothesis that says debt monetization should create both inflation and high nominal interest rates.

Lyn doesn't believe that the low-interest rates are natural.

Post global financial crisis, and with the uptake in quantitative easing, we've entered a different era where interest rates are less reflective of inflation. Central banks can take excess supply off of the market and distort interest rates.

She believes that we are already holding interest rates below their equilibrium level. How can we tell? Long-duration Treasury rates are still below the forward expectations you get from looking at the TIPS market. Alden thinks we are in this environment currently and that it is more of a question of magnitude than if this is the current state of affairs.

Because we don't have a developed country that has not done quantitative easing, we don't have any sample without it, where there hasn't been intervention, and interest rates went down to these very low levels. It could be a hybrid situation, where fed policy promotes increased debt, constrains growth, and puts downward pressure on rates in the future.

Is inflation transitory?

Scott believes should be concerned about inflation but it will most likely return to somewhere around a 2% average for the next decade.

He believes we should rely on market signals (TIPS spreads), which indicate that hyperinflation is unlikely. Market signals are the "least bad" prediction. Monetary policy is probably too expansionary right now because we are on track to exceed the Fed's 2% inflation target, but it is unlikely we'll have anything like hyperinflation. Scott is even confident that inflation will not exceed 3% for the decade. The Federal Reserve has the capability and the political will to adjust monetary policy to slow growth and spending.

Lyn believes that inflation will be significantly higher (somewhere above 3% a year) over the next decade.

She is skeptical of market signals and finds them unreliable and prone to manipulation. For example, during the European sovereign debt crisis, the ECB was willing to come in and buy bonds as needed, to fix that supply-demand mismatch distorting market signals.

What role do commodity cycles play in inflation?

Lyn believes that commodity cycles play a large role in inflation.

She finds the importance of real-world constraints is important. Commodities tend to go on massive, 10-year cycles because companies in commodity markets don’t control the price of their product, as commodity markets are perfectly competitive.

Within a commodity cycle, you have a period where commodity prices are high, where there is either too much demand or not enough supply. Prices go up, which encourages new producers to enter the market. Then you get either a slowdown in demand, or you just bring in so much excess supply to the market that you flood the market, creating a structural period of oversupply.

Because you have capital-intensive assets like big mines or oil fields, oversupply can last for many, many years. The same thing can occur with periods of undersupply because it can take years to bring online new productive assets. This means that you tend to go through large commodity cycles, and you generally see a bigger disconnect between the money supply and inflation during these periods.

Scott’s believes commodity cycles are essential for understanding inflation, but only for short-term cycles:

Scott thinks nominal GDP growth does a better job of explaining longer-term inflation than commodity cycles do.

Globalization

What is Triffin's dilemma? What are some of the pros and cons of being the global reserve currency?

Triffin's dilemma states that having a reserve currency gives a country tremendous power while at the same time putting a curse on it that guarantees that such a position cannot last forever. A country that issues a reserve currency must balance its interests with the responsibility to make monetary decisions that benefit other countries. If another reserve currency replaces the dollar would increase borrowing costs, which could impact the United States' ability to repay debt.

Robert Triffin believed the dollar could not survive as the world's reserve currency without requiring the United States to run ever-growing deficits. Having a popular reserve currency drives up its price and lifts its exchange rate, which hurts the currency-issuing country's exports, and leads to a trade deficit.

Lyn sees the Triffin's Dilemma as a dilemma the United States currently faces.

Having the reserve currency means you have to supply enough dollars to the world to use the currency. She sees several advantages to having the global reserve currency. These include global reach and the ability to sanction other countries. Some cons are that trade deficits get cycled into financial assets, propping up asset prices, and driving inequality.

Sumner doesn't believe that the advantages of being the global reserve currency are as significant as Alden thinks.

He notes that the US can indeed borrow money very cheaply at 1% or 2% interest rates. We can maintain trade deficits because of the difference in the rate of return from what we earn on foreign investments vs. what foreigners are earning on treasury bonds. It's unclear if there will be a day of reckoning in the future.

How special is the Dollar’s status as the global reserve currency? It does have some advantages, and it affects the size of our trade deficits, but the size of the effect is unclear, and almost all developed countries today can borrow at very low interest rates now.

How big of a problem are trade deficits?

Scott doesn't believe that trade deficits are much of a problem.

He believes that we are a long way away from a "day of reckoning" regarding trade deficits in the United States. Although the net international investment position is increasing, it isn't at a level that is too high at the moment. He believes that a day of reckoning might not even be a bad thing. It might force Americans to cut consumption and austerity. Still, it could also increase the manufacturing base in the United States.

Lyn believes that trade deficits are a problem.

She agrees that a day of reckoning might not necessarily be a bad thing. However, she does note that the net international investment position has gone exponential, ie, it's accelerating very fast and is increasing at a rate that is not sustainable. The day of reckoning could be closer than we realize.

US and China: who has more leverage in the relationship?

Lyn believes that the relationship is relatively symmetrical.

Both countries have insurmountable advantages over each other, hence, both countries are intertwined. The United States has great geography, deepwater ports, water borders instead of land borders, and lots of commodities. On the other hand, the United States has a poor manufacturing base and a net negative international investment position

China has an extensive manufacturing infrastructure, something that is very important if the trend towards less globalization continues. China does have problems accessing commodities, but its Belt and Road initiative helps solve some of those problems. Additionally, China has a net positive international investment position and they continue to buy up dollar-denominated assets by running structural surpluses. On the other hand, China has very poor demographics and many land borders to police.

Scott believes that the United States might have a bit more leverage.

The biggest advantage the United States has is an exceptional pool of talent. Because of this, the country is good at doing things other countries are not, like building tech companies (Silicon Valley) and making great movies (Hollywood). He believes that the anomalous trends with trade deficits in the United States are primarily due to the United States' massive wealth.

Scott thinks it is likely that China could work very hard and save a lot but not get rich. It could go like the US or just end up like Germany or Japan. Germany is a great example, Germans work very hard and save a lot, but they never invest their money, instead preferring to put it into savings accounts, so they don’t get as wealthy. Therefore, China's success rests on its human capital and whether it implements a dynamic economic system. If China invests wisely and implements good policy, it will be successful. If they follow the Germany/Japan model, they won't catch up to the United States.

Conclusion

In summary, Alden and Sumner broadly agree on most points. They both agree that the current level of debt is a problem and will have to be paid for in the future. Both Sumner and Alden think the 1940s are a good model for today's situation regarding the national debt.

Alden believes the US will use inflation to reduce our debts, and Sumner believes we will experience higher taxes and austerity.

Sumner is skeptical that using inflation to reduce our debt is feasible at the scale required to reduce the debt substantially. He is generally more confident in the Fed’s ability to manage inflation should it need to. Alden is more skeptical about the Fed’s ability to manage inflation and expects that we will experience a period of much higher inflation over the next decade.

He believes that our current burst of inflation is transitory and expects the rest of the decade to converge with the Fed’s 2% inflation rate target. Alden believes that the market signals around inflation are misleading. Although Scott admits that market signals are not perfect, he believes they are the “least bad” predictions we have and is skeptical of much manipulation of market signals by central banks.

On globalization, Scott is generally less worried about trade deficits than Alden is. In terms of the US/China Conflict, Sumner thinks that the United States has a bit more leverage in the relationship with China and Lyn thinks the relationship is fairly symmetrical.

If you'd like to read more about any of these topics, read Alden and Sumner to learn more.

Thanks to Will Jarvis